A convict was in jail for decades. One day, not in July, he made an elaborate escape (think of the show Prison Break). He crafted a human-sized dummy of himself using his own hair to buy himself hours as he broke out of the prison.

Once he was outside the walls of the jail, he repeatedly stole cars and ditched them as they ran out of gas despite having access to wallets full of credit cards. Why?

As it turns out, in the decades since he entered jail, he was unaware of how electronic gas pumps operated including using credit cards to purchase gas. Ouch.

Investors can empathize. It feels like real-time information is the key to success. But is it possible that investors don’t know what to do with this information?

I’ve had conversations with investors of all experiences, backgrounds, wealth levels, etc. this year, and a few hot topics were commonly brought up that should be locked away once and for all.

“Market Timing” – Investors still believe they can do it. It is often prefaced with “I’m not trying to time the market, but…” and then leads into a data point as to why now is the time to do X or Y. It’s a fool’s errand that may lead to severely underperforming the market long-term.

“The Market Is Expensive” – This is the ultimate defense mechanism for any decision (not investing, selling, etc.). What’s the truth? Certain areas of the market are more expensive than their historical averages, but you shouldn’t extrapolate that to the entire world stock market. Even if an area of the market is “expensive,” is that a bad time to buy? The research shows investing only at all-time highs in the S&P 500 has an average return close to the index.1 Time in (not timing) the market matters.

You can buy inexpensive investments that may never return anything, and you can buy expensive investments that may return handsomely. The reverse is also possible. For an extreme example, if you bought Netflix at its peak Price to Earnings Ratio over 4502 (extremely expensive) in 2013 you would have seen a return of over 3,200% percent in the decade plus since.3

“Useless Information” – There is a ton of it and investors are gobbling it up at a rate that necessitates a GLP-1. One of my favorite hyper-focuses was the infatuation with Warren Buffet’s actions as a signal for market doom. He’s a historied investor, but he knows just as much about the future as the rest of us. Yet other “normal” investors read the tea leaves and concluded that Buffet knew something individual investors didn’t. Maybe yes, maybe no. It’s definitely a data point. However, is this information the signal or the noise? Is it possible that Buffett was freeing up cash for Berkshire Hathaway to buy out his shares from his estate should he pass away? Connecting dots is dangerous. Ironically, Warren Buffet himself says, “Forecasts may tell you a great deal about the forecaster; they tell you nothing about the future.” Maybe investors should listen to his advice instead of extrapolating from his actions.

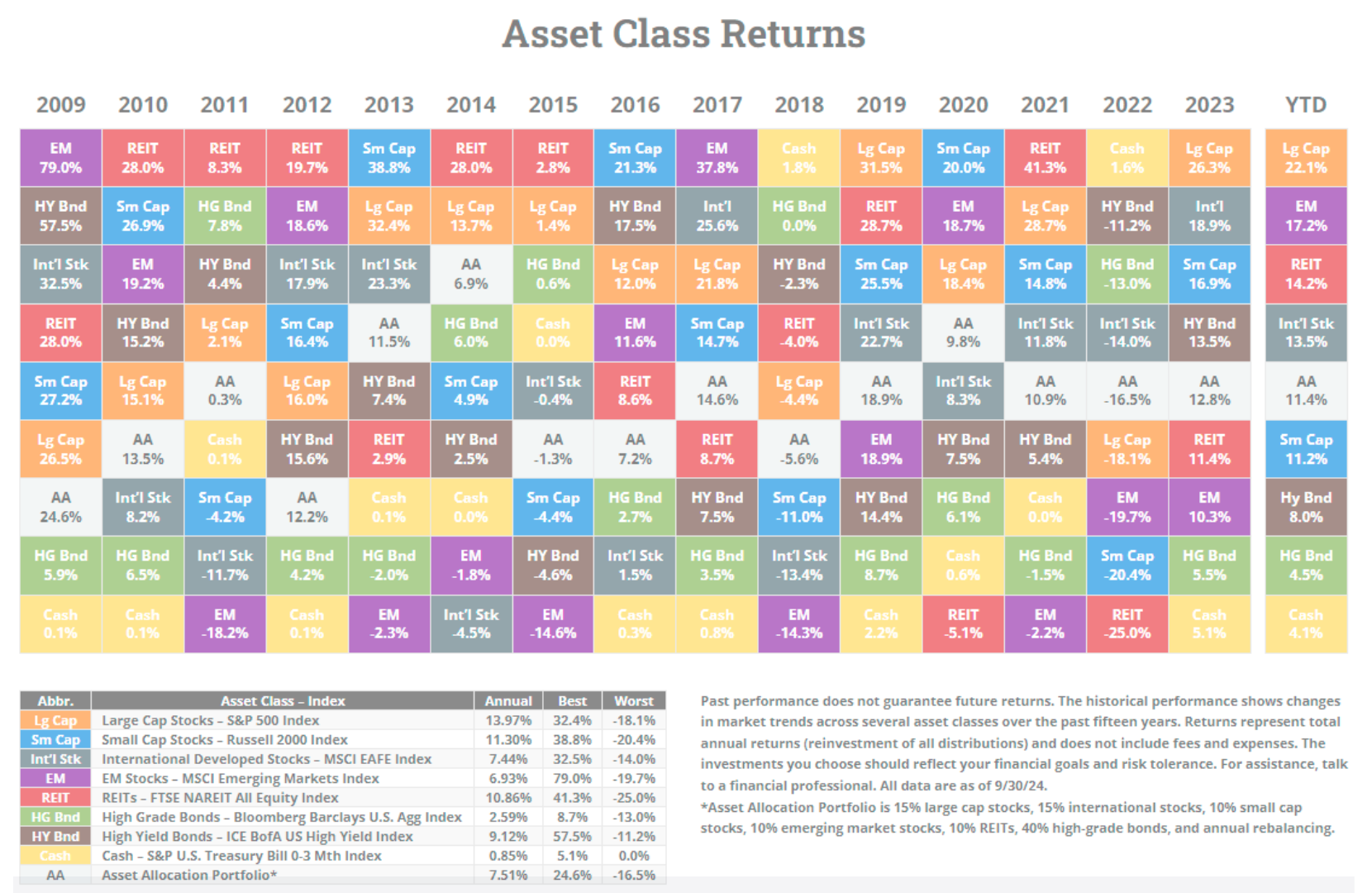

“Cash-Like Investments Are King” – Well they are more like the silly jester this year. The stock market again rewards those who are in the market. It really is that simple, but seemingly also that hard. Here’s what major asset classes returned through Q3 of 2024. History doesn’t favor cash-like investors either.

The overarching takeaway is that too many investors continue to suffer more in imagination than in reality.

If you were one of the many investors who bought and held index fund investments at your risk tolerance this year, congratulations! You should feel proud of your behavior and another successful year.